Travelzoo: Travel To Recovery Remains Long, But Hope Floats (NASDAQ:TZOO)

AscentXmedia/E+ via Getty Images

Travelzoo (NASDAQ: TZOO) was one of the hardly-hit companies amidst the pandemic. Deemed as non-essential, restrictions led to massive revenue cuts and net losses. It had to discontinue its Asia Pacific segment, contracting its operating capacity. But today, it continues to rebound with robust operations and higher user engagement. With the easing of restrictions, travel and leisure are now safer and more accessible. Statistics show more growth opportunities this year despite disturbances in Europe. Likewise, the stock price has renewed hope following a recent upside.

Company Performance

Travelzoo shows more promise this year with the rebound in its core operations. After cutting its costs and discontinuing its Asia Pacific segment, its revenues decreased. But, it helped reduce costs and expenses amidst tighter restrictions and competition. So, 2021 ended with a 17% revenue rebound, positive operating margin, and net income.

The acquisition of Jack’s Flight Club was also an excellent move, focusing more on flight deals. The commission and advertising business model extended to cheap flight deals finder. This segment enabled subscribers to avail of its services for a reasonable annual fee. It is no wonder that it appears to be more lucrative due to recurring revenues.

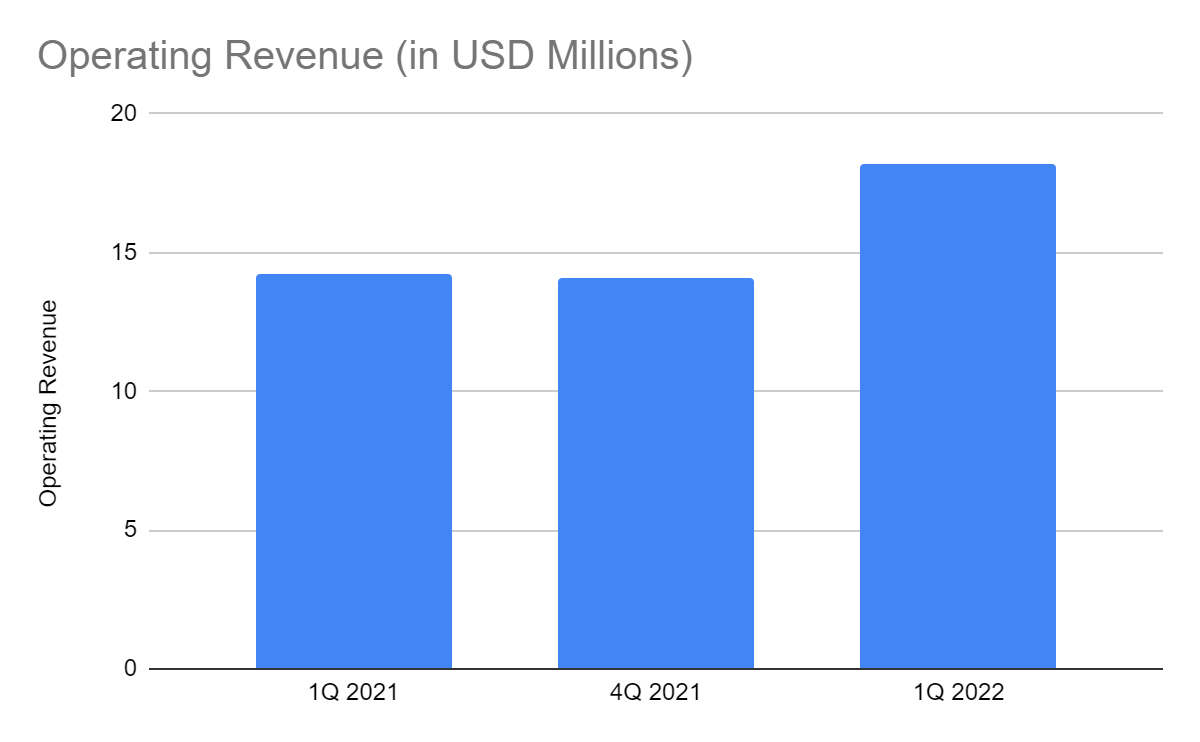

Today, Travelzoo is on its way to recovery, moving faster and further than expected. In its 1Q 2022 results, the operating revenue amounted to $18 million, a 28% year-over-year growth. Both its North America and Europe segments had substantial revenue growth. Thanks to the continued vaccination and easing of restrictions. The 2% increase in membership is also helpful.

Operating Revenue (MarketWatch)

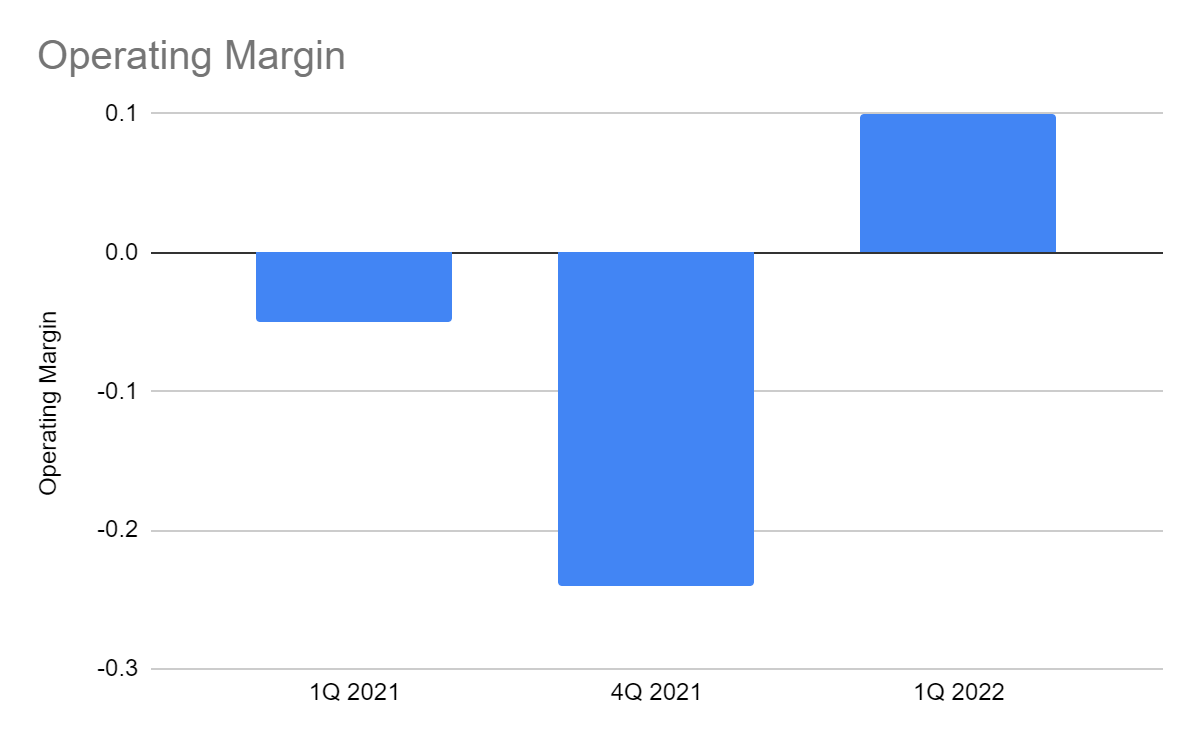

Moreover, Travelzoo has also become more efficient. So as it started to expand again, it kept its costs and expenses low. The operating margin is now 10%, the highest since the pandemic hit the company.

Operating Revenue (MarketWatch)

Potential Challenges and Growth Opportunities This Year

Travelzoo still has to sustain its recovery and bounce back from pre-pandemic levels. The Russo-Ukrainian War is another deterrent due to the apprehension it brings. In a recent survey, 40% reconsider their travel plans due to the invasion. The effect of the war is still visible as travel and hotel occupancy rates dipped by 1.3% in March.

Despite this, hope floats as more people are willing to travel this Spring and Summer. In the same survey, 65% of Americans were more willing to pay higher fees to reach their destinations. It shows the firm determination of the vast majority to go out and travel. Indeed, consumer behavior plays a vital role in its recovery and growth this year. The lower transmission rate in many other countries gives travelers more confidence.

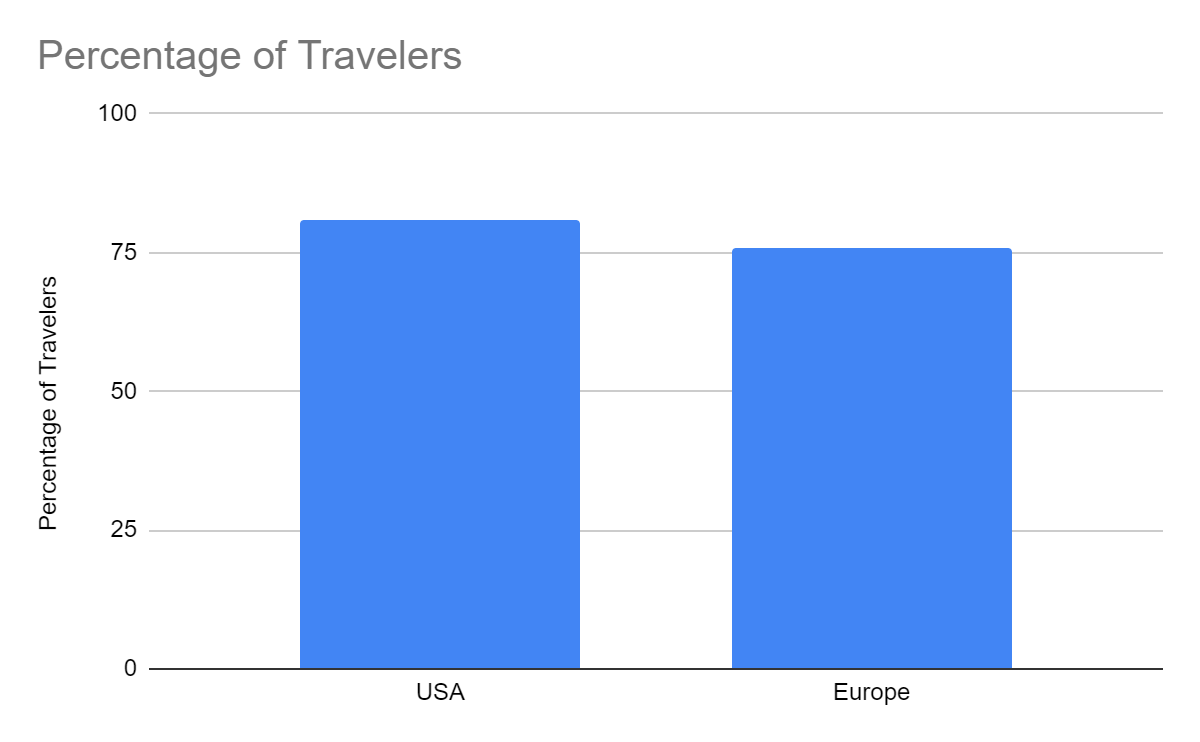

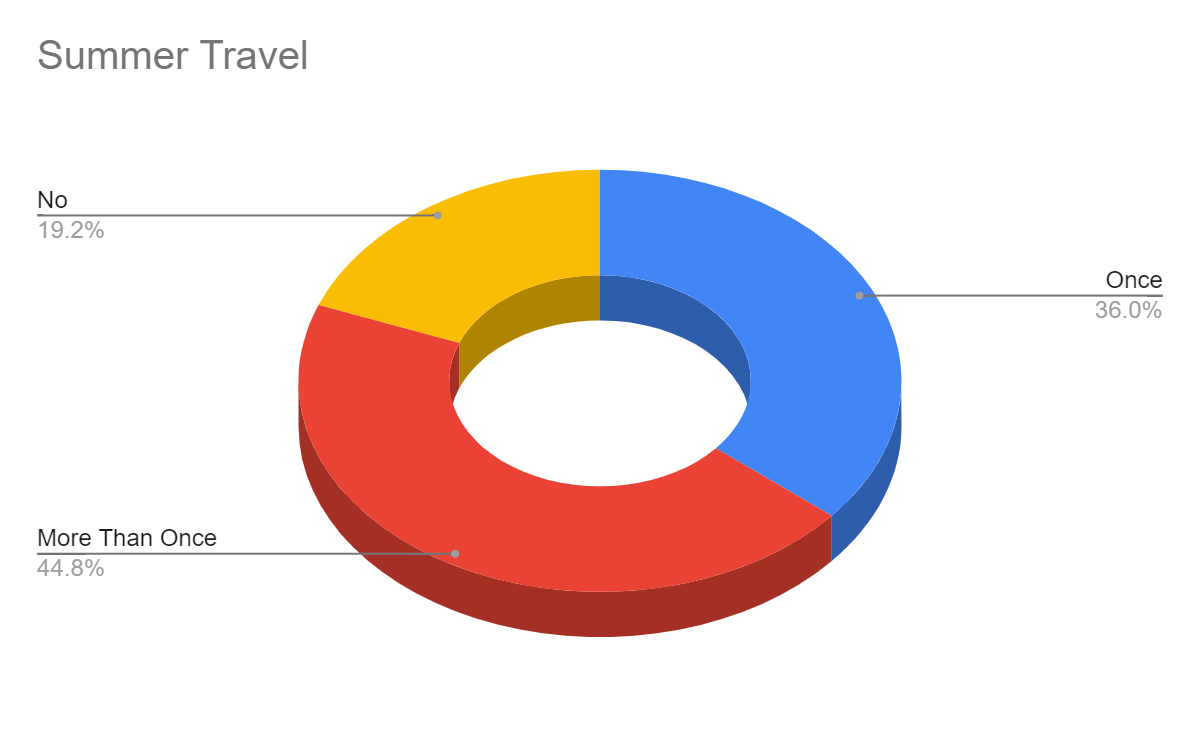

On TravelDailyNews, 203 million Americans plan to travel this summer. It corresponds to 81% of the total population, a 13% year-over-year growth. Among them, 36% will travel once, while 45% will travel more than once. Meanwhile, 51% plan to travel by plane, and almost half of them will board more than once. Europe also shows a rosy future amidst the ongoing war and the decrease in the transmission rate. In a recent survey, over 70% of Europeans may travel this Spring and Summer. Over 50% will only travel in the region. Those residing in Italy, Spain, Germany, Poland, and the UK are the most optimistic.

Percentage of Travelers (TravelDailyNews)

Summer Travel (TravelDailyNews)

It is indeed a good opportunity for Travelzoo to cater to a wider audience.

Jack’s Flight Club may see increased demand as more people fly to other cities and countries. This app may provide subscribers with cheaper flight deals as air traffic rises. With its concentration in North America and Europe, it can capture more demand in the core market. As of now, it already has 1.7 million subscribers, a 6% increase from March 2021. Note that most of them are from Europe. Also, flights in the US and Europe comprise 96% of revenues. So, the increased appetite for European travel will benefit the company.

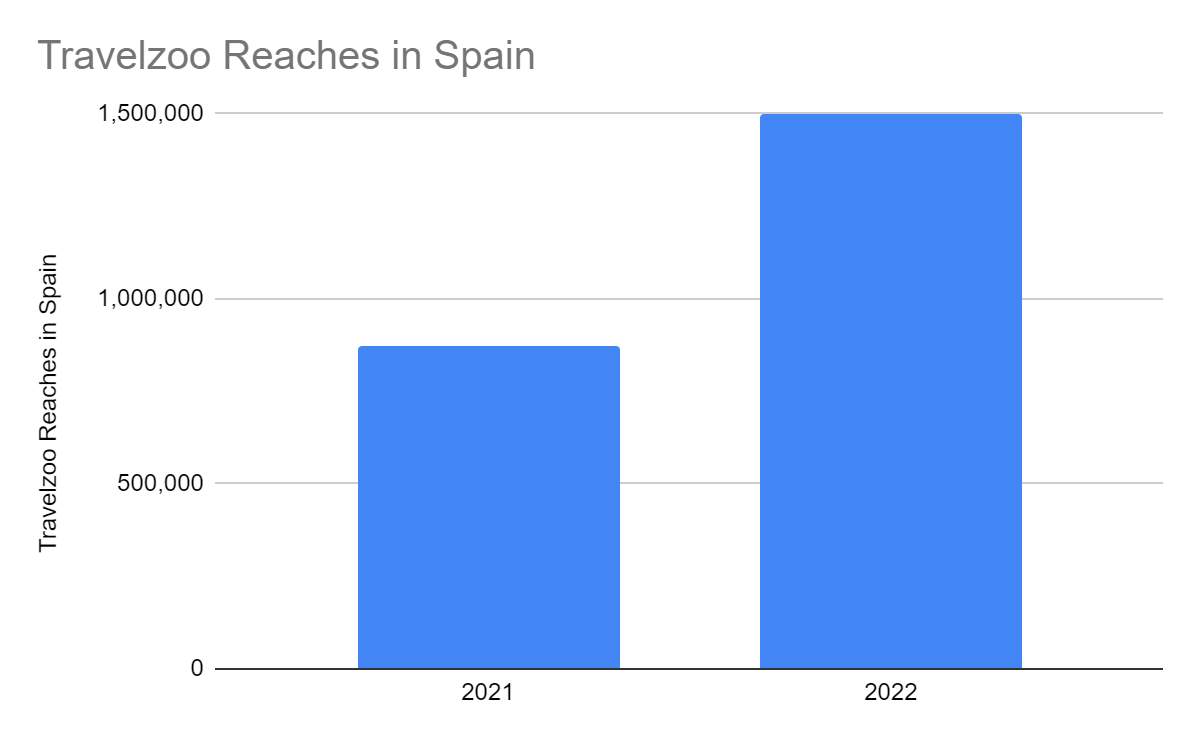

The acquisition of Secret Escapes also appears timely. It will help boost its market concentration in the region. It can cater to more Europeans and generate more leads. In a short period, it proved fruitful as the number of reaches had a dramatic increase. In Spain alone, the number of travel enthusiasts it now reaches is already 1.5 million, 72% larger than before. Even better, Spain is one of the most favorite destinations in Europe. Even most Travelzoo members favor this country. So, user engagement, particularly in the country, may go up this summer. It may be able to capture more users and raise rates without sacrificing efficiency. Metaverse may improve the user experience with more exclusive deals for members. It may also increase its partnerships with travel and accommodation suppliers.

Travelzoo Reaches in Spain (Travelzoo Press Releases)

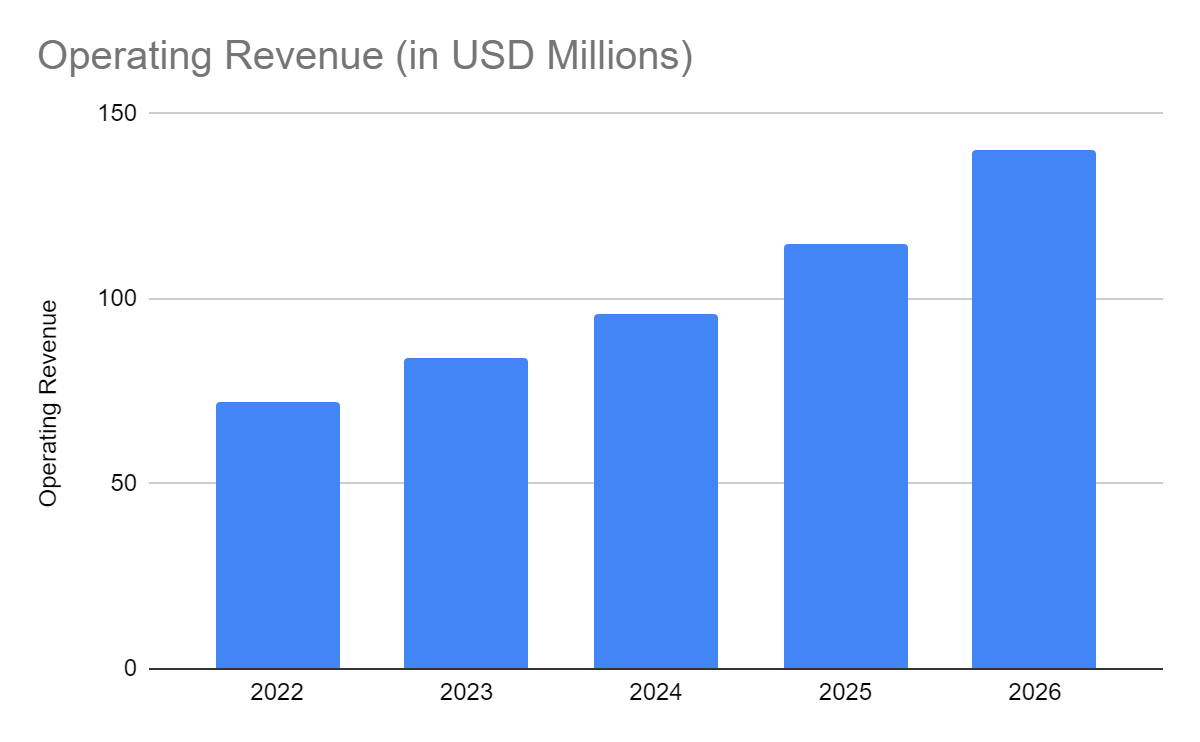

Travelzoo may generate more revenues while keeping its costs and expenses manageable. With more business segments, it can diversify its services for more reach and leads. It is possible as more people seek to travel. In the previous year, the Delta variant disrupted the recovery. It became more transmissible and scarier. But now, it has more opportunities as the pandemic fear subsides. This year, I project a continued increase in the operating revenue. But given the war and pandemic uncertainties, the increase may not be as large as 1Q 2022. I project a 16% increase in 2022-2024 and a 20% increase in 2025-2026.

Operating Revenue (Author Estimation)

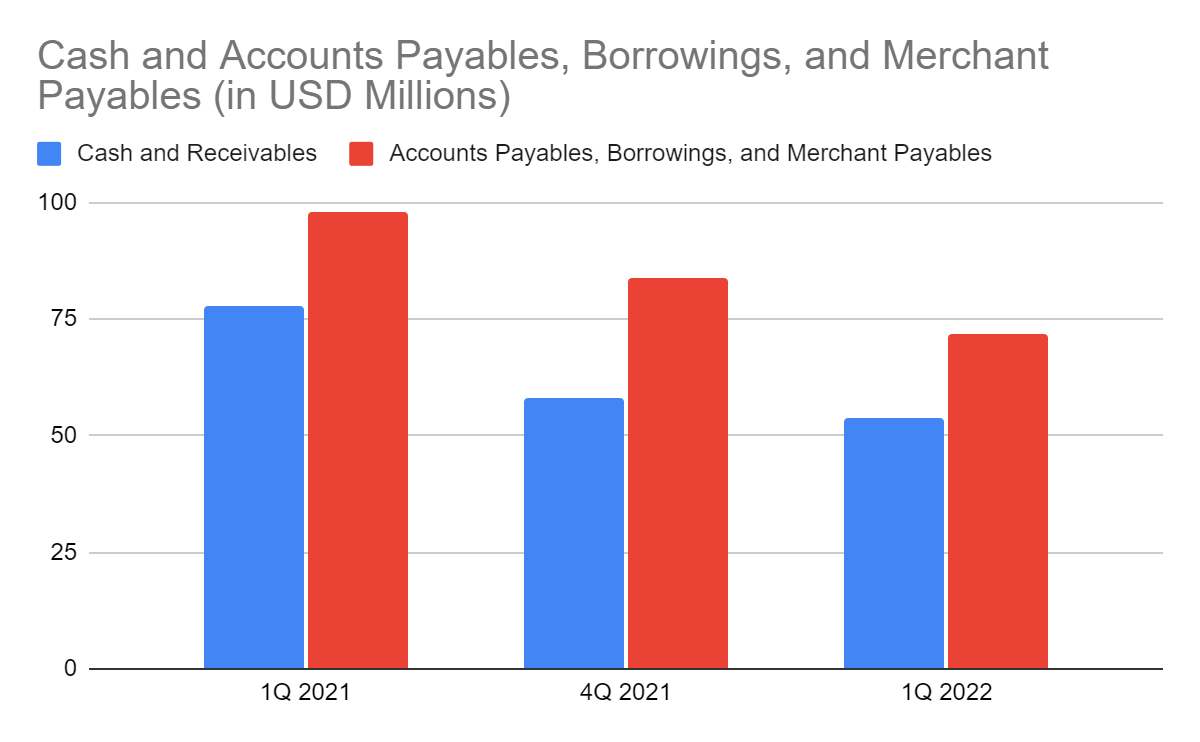

Moreover, Travelzoo has better fundamentals, showing the consistency between profitability and liquidity. Its cash balance dropped by almost 50%, but payables and borrowings decreased as well. It remained in line with its goal to focus on performing segments. Also, it was driven by more members redeeming vouchers. In turn, the operating revenue and net income increased. The current financial position shows more stable fundamentals. It has the means to enlarge its capacity with more demand and efficient asset management. It is more profitable and sustainable, allowing it to expand as the industry continues to hype up.

Cash, Receivables, Borrowings, and Payables (MarketWatch)

Stock Price

The price has been in a sharp decline since the second quarter of the previous year. It was quite a shock since the idea of travel and leisure rebound was appealing. But, the external pressures put downward pressure on the stock price. Also, earnings were still not matched with the stock price. Inflationary pressures and Omicron pushed it down further. But after the release of the 1Q 2022 report, the stock price had an upside of 14% to $7.18. Given the EPS of $0.19, the TTM value increased by five times. So, the P/E Ratio dropped by more than five times as well. At 18.89x, the stock price appears fairly valued. So, the new price increase is more reasonable now. To verify this, I used the DCF Model using the FCFF method.

|

FCFF |

$3,500,000 |

|

Cash and Equivalents |

$42,000,000 |

|

Outstanding Borrowings |

$12,000,000 |

|

Perpetual Growth |

4.40% |

|

WACC |

9.60% |

|

Common Shares Outstanding |

12,000,000 |

|

Stock Price |

$7.18 |

|

Derived Value |

$8.16 |

The derived value shows that there may be a 12-14% upside for the next 12-24 months. It may be possible, given its profitability this quarter. But of course, pandemic uncertainties and the ongoing war must also be considered. Nevertheless, the P/E Ratio and the DCF model suggest that the stock price is fairly valued.

Bottomline

Travelzoo may still take a long path to recover fully. But its improvement in 2021 and the impressive 1Q 2022 financials show hope for a rebound. The return of travel demand may help it operate at a larger capacity. Meanwhile, the stock price remains low with no promise of an immediate upside. The cheapness and growth opportunities may be a good combination. The recommendation is that Travelzoo is still a buy.